Article Summary:

- Restructuring an LLC or S corporation into a C corporation can be part of a strategy to pursue QSBS treatment, but only if QSBS-eligible stock is properly issued under Section 1202.

- When structured correctly and held for the required period, QSBS can allow up to $10 million (or 10x basis) of federal capital gains to be excluded on a future sale.

- This approach is most relevant for business owners planning long-term growth, outside investment, or an eventual liquidity event.

- Any restructuring should be evaluated carefully against tax, governance, and succession trade-offs and coordinated with broader business and estate planning.

If you’re running a successful California business and thinking ahead to a future sale, one question tends to surface sooner than expected: Is the current business structure still the best long-term choice?

Many owners form LLCs or S corporations early on for simplicity or short-term tax efficiency. But as revenue grows and conversations shift toward scaling, acquisitions, or a future exit, those early decisions don’t always align with long-term goals.

At that stage, Qualified Small Business Stock (QSBS) under Internal Revenue Code §1202 often enters the conversation. The potential upside is significant. When structured correctly, QSBS can allow up to 100% exclusion of federal capital gains tax on the sale of stock, subject to statutory limits. For owners planning a future liquidity event, that can materially change the after-tax outcome.

The key issue isn’t simply whether you convert your entity. It’s how and when QSBS-eligible stock is issued and whether your restructuring actually qualifies under the rules. QSBS treatment is tied to the issuance of qualifying C-corporation stock—not the act of converting an existing entity.

The most effective approach is to convert to a C corporation and then issue qualifying C-corp stock that is eligible for QSBS treatment to shareholders under Section 1202.

What QSBS Means for Your Business?

QSBS refers to stock issued by a domestic C corporation that meets specific requirements at the time the stock is issued.

If your stock qualifies and you satisfy the holding period and other rules, Section 1202 may allow you to exclude up to the greater of $10 million, or 10 times your tax basis in the stock from federal capital gains tax upon sale.

This exclusion applies only to qualifying stock issued by the corporation. It does not apply retroactively to ownership interests that existed before QSBS-eligible stock was issued.

At a high level, QSBS eligibility generally requires that:

- The company is a domestic C corporation at the time the stock is issued

- Gross assets do not exceed $50 million immediately before and after issuance

- The company operates an active trade or business

- The stock is held for more than five years

If these requirements are met, QSBS tax treatment can substantially improve the economics of a future exit.

Why QSBS Requires More Than a Simple Conversion

The most effective QSBS strategy is not conversion alone. It is the issuance of qualifying C-corporation stock after the business is operating as a C corporation.

QSBS benefits apply only to stock that meets the original-issuance requirements of Section 1202. That means the focus of planning is on how and when C-corp stock is issued to shareholders, not simply on changing the entity’s tax classification.

In practice, this often involves restructuring the business so that, once it is operating as a C corporation, new stock is issued that can begin the QSBS holding period. From that point forward, shareholders who hold the stock for more than five years and meet the other statutory requirements may be eligible for the QSBS gain exclusion.

This distinction matters. A conversion may be a necessary step, but it is the issuance of qualifying C-corp stock that determines whether QSBS treatment is available in the future.

Here is the critical clarification for LLC and S corporation owners: QSBS applies only to stock issued by a C corporation, and only to stock that qualifies as original issuance.

That means:

- LLCs and S corporations cannot issue QSBS

- Simply converting an existing entity to a C corporation does not automatically make previously held ownership interests QSBS

- QSBS treatment generally begins only when qualifying C corporation stock is issued under the rules

In some cases, owners explore F reorganizations or other restructuring strategies designed to preserve continuity while allowing new QSBS-eligible stock to be issued going forward. These transactions are highly technical and must be structured carefully to avoid disqualifying the stock.

The takeaway is straightforward: QSBS planning is not a check-the-box conversion. Timing, structure, and issuance mechanics matter.

Common Reasons Business Owners Convert from LLC or S Corporation

When done correctly, restructuring can open planning opportunities that simply don’t exist in pass-through entities.

- Better After-Tax Exit Outcomes

QSBS can dramatically reduce federal taxes on a future sale. With careful planning, owners may also be able to:

- Allocate QSBS stock among spouses, trusts, or family members

- Multiply available exclusions within statutory limits

- Align business exit planning with estate planning objectives

Because the five-year holding period begins when QSBS-eligible stock is issued, early planning matters.

- Alignment With Investors

Many investors prefer C corporations due to:

- Familiar governance and equity structures

- Clear exit mechanics

- Potential QSBS eligibility on new stock issuances

If outside capital is part of your growth plan, restructuring earlier can reduce friction later.

- Equity and Succession Flexibility

C corporations allow greater flexibility in:

- Issuing equity to key employees

- Designing long-term ownership structures

- Coordinating succession planning with tax strategy

When paired with QSBS planning, these tools can support both growth and legacy goals.

What You Give Up When You Convert?

Restructuring toward a C corporation structure in pursuit of QSBS eligibility is not a one-way upgrade. It involves real trade-offs that affect how your business operates, how you access cash, and how much flexibility you retain year to year.

Loss of Pass-Through Tax Treatment

LLCs and S corporations offer pass-through taxation, meaning income and losses flow directly to your personal return. Many business owners rely on this structure to:

- Access earnings through distributions

- Use certain losses to offset other income (subject to limits)

- Maintain flexibility in how and when income is recognized

Once you operate through a C corporation, that model changes. The corporation pays its own tax on profits, and shareholders may be taxed again when funds are distributed. This “two-layer” tax system can feel inefficient in the short term, particularly for owners who rely on annual distributions to support their lifestyle.

Reduced Flexibility in Annual Tax Planning

C corporations operate under more rigid tax rules. You lose some of the ability to fine-tune your personal tax outcome each year through distribution timing, entity-level deductions, or income allocation. For owners accustomed to actively managing annual tax exposure, this shift can feel restrictive, even if the long-term exit math looks favorable.

Increased Administrative and Governance Requirements

C corporations require more formal structure:

- Board and shareholder actions

- Stock issuance and tracking

- Corporate minutes and records

- Clear separation between ownership and management

These requirements are manageable, but they represent a meaningful change from the flexibility many owners enjoy in LLC or S corporation structures. If simplicity and minimal administrative burden are priorities, this factor deserves careful consideration.

Short-Term Cost for Long-Term Optionality

Restructuring often introduces legal, accounting, and compliance costs well before any QSBS benefit materializes. The potential reward comes later, at exit, and only if the business ultimately qualifies and performs as expected.

This is why restructuring should be viewed as long-range positioning, not immediate tax relief.

Signs You’re Ready to Convert to a C Corporation

Restructuring toward QSBS eligibility is not about optimism alone. It’s about realistic growth expectations and strategic timing.

You may want to take a deeper look if several of the following apply:

You’re Building Toward a Liquidity Event

If a sale, recapitalization, or other liquidity event is likely within the next 7–12 years, QSBS planning becomes more relevant. The five-year holding period means decisions made today directly affect options available later.

You Expect Meaningful Appreciation

QSBS matters most when appreciation is substantial. If your business could realistically exceed current value by a wide margin, the ability to exclude a portion of that gain from federal tax can materially change your net outcome.

Your Business Has Outgrown Early-Stage Structures

As companies grow into the multi-million-dollar revenue range, early entity choices sometimes start to constrain:

- Investor conversations

- Equity compensation planning

- Long-term succession strategies

At that point, owners often revisit structure not because the original choice was wrong, but because the business has evolved.

You’re Thinking Beyond Your Own Ownership

If part of your goal is transferring value to family members, trusts, or the next generation, restructuring may support more thoughtful planning. When combined with estate planning, equity restructuring can align business growth with long-term family security.

You’re Willing to Trade Short-Term Efficiency for Long-Term Outcomes

Restructuring rarely improves short-term cash flow or tax simplicity. It makes sense only if you’re comfortable giving up some annual flexibility in exchange for stronger positioning at exit.

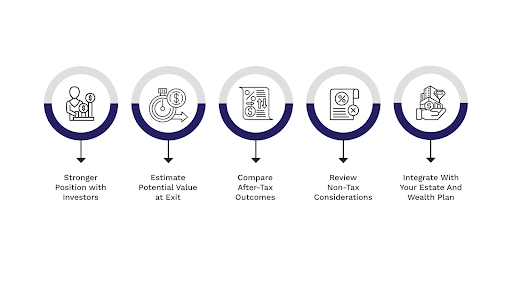

Best Practices for Evaluating a Move to a C Corporation

The most common mistake owners make is treating this as a narrow tax question. It’s not. This is a planning decision that sits at the intersection of business growth, tax strategy, and succession.

A disciplined evaluation includes several steps.

- Define Your Likely Exit Paths

Start by being honest about your long-term intent. Are you:

- Building to sell to a third party?

- Planning a private equity transaction?

- Hoping to pass the business to children or key employees?

Each path places different demands on structure, timing, and tax strategy.

- Model Realistic Valuation Scenarios

You don’t need precision, just reasoned estimates. Understanding whether a future sale could be $5 million, $15 million, or significantly more helps determine whether QSBS planning would move the needle.

- Compare After-Tax Outcomes Across Structures

This means comparing:

- Staying in a pass-through entity

- Restructuring to a C corporation and issuing QSBS-eligible stock going forward

The goal is not theoretical savings, but a clear picture of net results under realistic assumptions.

- Factor in Non-Tax Consequences

Consider how restructuring affects:

- Control and governance

- Investor expectations

- Employee equity plans

- Administrative workload

- Family involvement in ownership

These factors often matter as much as the tax outcome.

- Coordinate with Estate and Succession Planning

Finally, integrate the analysis with your broader wealth plan. For many owners, the most powerful planning happens when business structure, trust planning, and family goals are aligned rather than handled in isolation.

Get Expert Guidance on QSBS and Conversion for Your Business

QSBS rules are technical. The QSBS eligibility analysis depends on your industry, your asset levels, your timing, and how your corporate documents are drafted. The mechanics of an LLC-to-C-corporation conversion also vary by state law and by how your current entity is set up.

Because of this, you should:

- Work with a tax counsel who understands QSBS

- Coordinate with your CPA and financial advisor

- Make sure any conversion of an LLC to a C corporation is done correctly, so you don’t accidentally miss QSBS treatment later

If you’re evaluating whether a conversion to a QSBS-eligible C corporation aligns with your growth or succession goals, Dahl Law Group can help you assess the long-term implications for your business and your family.

Review your ownership structure today to ensure it fully supports your long-term financial, estate, and succession planning goals.

FAQs

- Can an existing LLC or S corporation qualify for QSBS without converting to a C corporation?

- Does converting to a C corporation restart the QSBS five-year holding period?

- Will converting trigger taxes at the time of conversion?

- Does QSBS eliminate all taxes on the sale of the business?

- Is QSBS only relevant if I plan to sell the entire business?

Dahl Law Group

Latest posts by Dahl Law Group (see all)

- How California’s Single-Enterprise Rule Impacts Your Business - April 24, 2026