It’s common for parents to want to make things simpler for their children when it comes to inheriting what they’ve built.

Many Californians, however, believe that adding a son or daughter to the title of their home will spare them from the hassle of probate or complicated estate issues. Still, it actually creates more financial risk than necessary.

On paper, it sounds easy. Just update the deed and be done with it. But that single decision can create tax headaches, expose your home to other people’s financial problems, and undo years of careful planning.

What you need is a Generational Wealth Protection Trust that empowers you and your children’s futures, rather than putting them at risk.

Before you sign anything, it’s worth understanding what actually happens when your child’s name joins yours on the title. This blog explains exactly why adding children to a deed, though common, can lead to significant tax burdens, title complications, and estate planning failures.

Article Summary:

- Adding children to a home title can have unintended consequences. What may seem like a simple way to avoid probate can actually create significant tax liabilities and expose the property to your child’s financial risks.

- Tax issues are significant. Transferring ownership may trigger gift taxes, capital gains taxes, or property tax reassessment under California’s Proposition 19.

- Joint ownership removes control and protection. A child’s debts, divorce, or lawsuits could jeopardize your share of the home.

- Better options exist. Trusts, transfer-on-death deeds, and other estate planning tools can protect your home while keeping your family’s financial future secure.

How Deeding Property to a Child Can Create Costly Tax Surprises?

Transferring ownership of your home to your children may seem like a thoughtful move, but when you add a child to the deed, you’re giving away ownership now, not later. This seemingly simple change can trigger significant tax consequences, impact your property’s future value, and create long-term liabilities under both federal and California laws.

Let’s break down the overlooked tax risks of deeding property to a child.

Immediate Tax Consequences of Transferring Ownership

When you transfer a deed to a child, the IRS considers it a gift. That’s because you’re giving away an ownership interest in a high-value asset without receiving anything in return.

Here’s how the tax implications of adding a child to a deed work:

- The value of the gifted share may exceed the annual gift exclusion limit ($19,000 per recipient for 2025).

- Anything over that amount counts against your lifetime gift and estate tax exemption (currently $13.99 million per person in 2025).

This triggers gift tax reporting requirements under California gift tax rules, which are based on federal law.

This doesn’t mean you have to pay a tax though – any amount you gift over the exemption amount is subtracted from your lifetime gift tax exemption amount.

Capital Gains Taxes When the Home is Sold

This is where many families get caught off guard. When a homeowner sells their primary residence, they may exclude up to:

- $500,000 of capital gains if married, or

- $250,000 if single

But this exclusion only applies to the original owner’s share of the property.

If your child is on the deed and does not live in the home as their primary residence, they will not qualify for the exclusion. When the house is eventually sold, their share may be fully taxable, resulting in significant capital gains tax.

Had you passed the home through an estate plan or trust instead, they likely would’ve received a “step-up” in cost basis, adjusting the home’s taxable value to its fair market value at the time of your death. This strategy often eliminates most, if not all, capital gains liability.

Property Tax Reassessment Under Proposition 19

California’s Proposition 19 limits parent-to-child tax advantages. If you add your child to the deed or transfer a deed to a child, the home may be reassessed at full market value, unless:

- The child moves into the property as their primary residence, and

- Files both the homeowner’s exemption and the parent-child exclusion forms

If these conditions aren’t met, your family could face a sharp increase in annual property taxes, completely wiping out the intended benefit of the transfer.

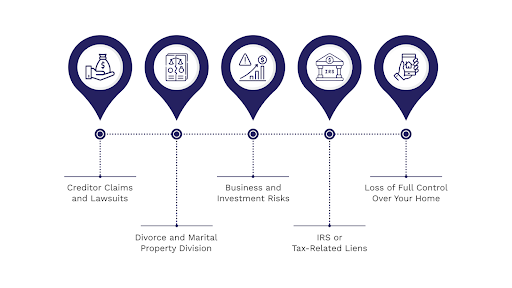

How Your Child’s Financial Liabilities Can Endanger Your Home?

Here are the critical liabilities that arise when you transfer a deed to a child:

- Creditor Claims and Lawsuits

If your child is ever sued or owes money, their share of the home becomes a target. Examples include personal injury lawsuits, unpaid business debts, credit card defaults, student loan delinquencies, and even minor claims disputes.

Once their name is on the title, your property becomes partially exposed to their creditors. Even if your child declares bankruptcy, their share of your home could be considered an asset for liquidation.

- Divorce and Marital Property Division

If your child gets divorced, their ownership interest in your home may be considered marital property, especially if the deed was transferred during the marriage. The couple invested in home improvements or paid related expenses.This means part of your home could be claimed by a former spouse, depending on how the court evaluates the situation.

- Business and Investment Risks

If your child owns a business, makes a poor investment, or takes on significant financial risk. Their assets, including their share in your home, could be seized to settle claims. In this case, deeding property to a child means that a failed venture or lawsuit could jeopardize your own financial security.

- IRS or Tax-Related Liens

If your child falls behind on income taxes or other obligations, the IRS or California Franchise Tax Board may place a lien on their ownership portion of the property. This may cloud the title and make it difficult for you to sell, refinance, or make decisions about the home.

- Loss of Full Control Over Your Home

Once your child becomes a co-owner, you cannot sell, refinance, or transfer the property without their permission. If your child disagrees with a decision, you may be legally blocked from acting.

This loss of autonomy is a common regret for parents who transfer a deed to a child too early. Even in the absence of financial issues, conflicting opinions between co-owners can delay or derail plans.

Gift Tax Limits When Deeding Property to a Child

Many homeowners don’t realize that adding a child to a deed is considered a gift under IRS rules. The IRS allows you to gift up to $19,000 per recipient per year (as of 2025) without having to file a gift tax return. This is known as the annual gift tax exclusion.

If you transfer a deed to a child and the value of their share exceeds $18,000, the excess counts against your lifetime gift and estate tax exemption.

From a tax perspective, adding children to a deed is not a symbolic gesture; it’s a reportable transfer of real property. The transaction might seem informal, but to the IRS, it’s a reportable transfer.

Practical Alternatives to Naming Your Children in the Title of Your Home

There are far better ways to make sure your home ends up where you want it.

- A revocable living trust is often the cleanest solution. You retain full control during your lifetime, and your children inherit the property directly upon your death, without the need for probate and with fewer tax surprises.

- Another simple option is a transfer-on-death deed, which automatically transfers ownership to your chosen beneficiaries upon your death.

- Families with higher-value homes may also consider tools such as qualified personal residence trusts (QPRTs) or limited liability entities, which balance protection with flexibility. The right choice depends on your goals, your assets, and how you want to protect your family’s future.

Pros and Cons of Adding a Child to a Deed

Understanding the pros and cons of adding a child to a deed helps homeowners see the full picture.

Pros

- May avoid probate

- Establishes immediate ownership rights

- Creates a clear succession path

Cons

- Triggers gift tax reporting

- Eliminates step-up in basis

- Risks of property tax reassessment

- Exposes the home to the child’s creditors

- Reduces parental control over the property

- Can complicate refinancing or selling

- May create family conflicts

The pros and cons of putting a house in a child’s name are rarely balanced; the potential downsides tend to outweigh any convenience.

Make a Well-Informed Decision Before Transferring Your Home

Adding a child to a deed may feel like a straightforward solution, but the tax and legal consequences can be significant. Understanding the inheritance tax gift rules, Proposition 19, and potential liability risks ensures you make a decision that protects, not jeopardizes, your home.

At Dahl Law Group, we help California families protect what matters most through strategic estate planning, tax optimization, and asset protection. Our team can guide you through every step to ensure your home is transferred safely and strategically.

Dahl Law Group

Latest posts by Dahl Law Group (see all)

- How California’s Single-Enterprise Rule Impacts Your Business - April 24, 2026