Article Summary:

- Trustees need more than the trust document and require detailed financial, business, and family information.

- Provide a comprehensive financial overview that includes assets, liabilities, and business ownership.

- Share clear business succession plans, key employee details, and buy-sell agreements.

- Regularly update your trustee on significant changes in finances, family, or business.

- Protect business assets by structuring the trust to safeguard against creditors and family disputes.

As a business owner, your company is likely one of your most valuable assets, both financially and personally.

Ensuring its continuity and protection, especially in unexpected circumstances, is crucial not only for preserving your legacy but also for securing the future of your family and employees. One of the most effective tools in achieving this is a well-structured trust.

When you choose a trustee for your estate plan, you’re entrusting them with the responsibility of making decisions that align with your wishes.

But how much information should you share with them to ensure they fulfill that duty effectively?

Most people assume the trust document tells the trustee everything they need to know. In reality, trustees often need context, clarity, and ongoing information to carry out your wishes properly, especially when a business is part of the estate.

For owners balancing growth, family, and succession planning, the level of communication you maintain with your trustee can directly affect how well the trust performs in the future.

The Role of a Trustee in Estate Planning

A trustee plays a crucial role in carrying out your estate plan, and their responsibilities go beyond managing your assets. Legally, a trustee is obligated to act in the best interests of the beneficiaries and strictly in accordance with the terms of the trust document.

This includes ensuring that assets are distributed correctly, debts are paid, and taxes are filed. Trustees also have a fiduciary duty, meaning they must make decisions with the utmost care and loyalty, always prioritizing the intentions you outlined in the trust.

The duties of a trustee include managing your estate’s finances, maintaining clear communication with beneficiaries, and making essential decisions on asset distribution.

The Importance of Sharing More Than the Trust Document with Your Trustee

Your trust document is essential, but it doesn’t give your trustee the whole picture. They need context to make informed decisions. Here’s why:

- Financial Shifts: Your financial situation can change over time, and your trustee must understand how those changes affect the trust’s objectives.

- Business Changes: If you own a business, your trustee may need to step in to manage it in the future. Without clear direction, they may make decisions that don’t align with your vision.

- Family Dynamics: Your family’s needs and values play a huge role in how you’ve structured the trust. Communicating these values helps the trustee honor them accurately.

What You Should Share With Your Trustee for Effective Estate Management?

0

To ensure your trustee can carry out your wishes, provide them with the following details:

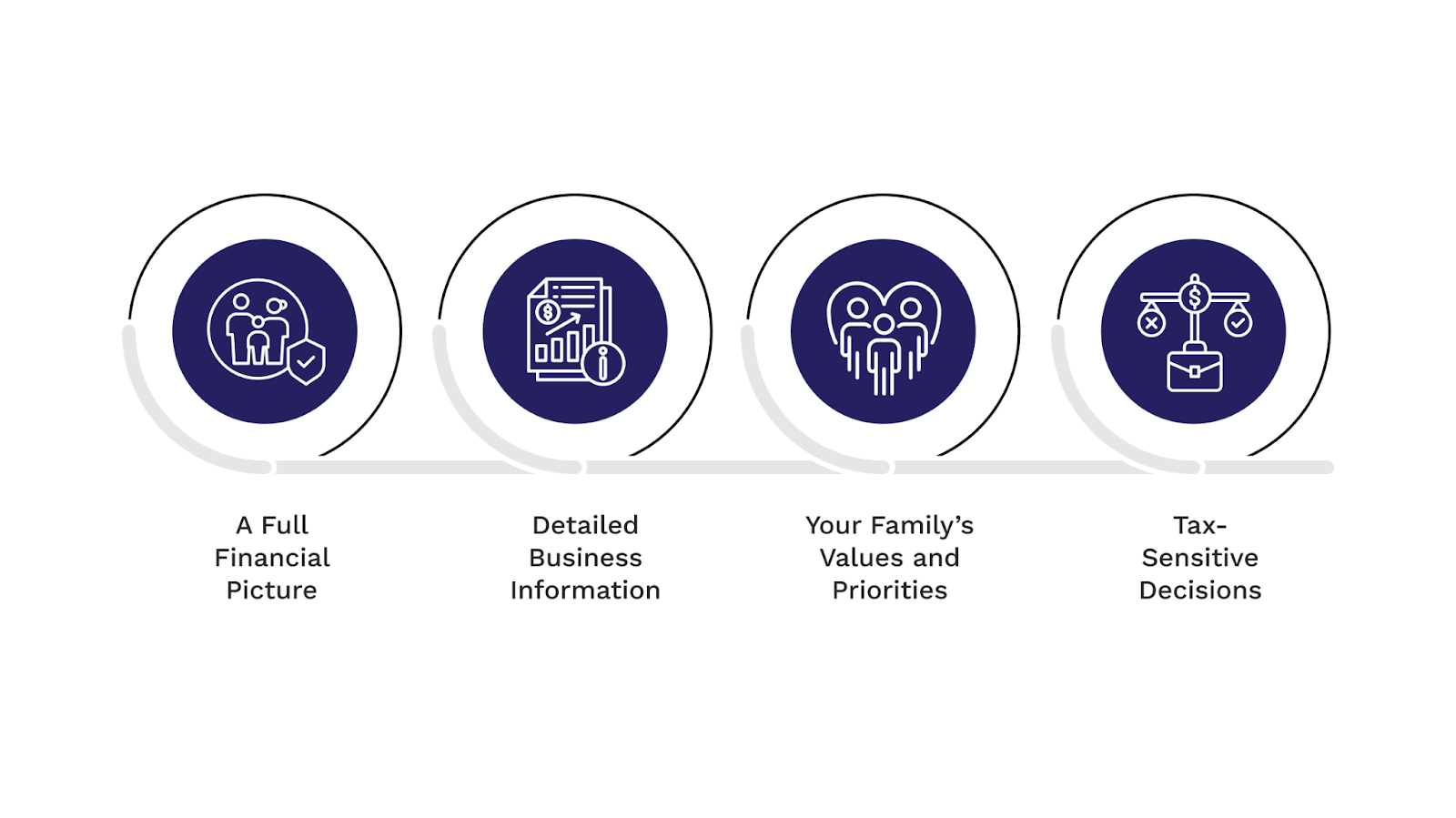

- A Full Financial Picture

Your trustee needs a comprehensive understanding of all assets and liabilities that fall under the trust. This includes:

- Business ownership

- Real estate holdings

- Retirement accounts

- Insurance policies

- High-value personal property

- Outstanding loans and obligations

By providing this information, you help your trustee make better decisions regarding the timing, liquidity, and risk management of these assets.

- Detailed Business Information

For business owners, this is a vital section. If your business is part of your estate, your trustee may be called upon to oversee a transition or sale. Share the following details:

- Your business succession plan

- Current business valuation documents

- Key employee details

- Operating and buy-sell agreements

- Specific instructions in case of your unexpected departure

This information will ensure your trustee isn’t left guessing how to proceed with your business.

- Your Family’s Values and Priorities

A trust isn’t just a financial document; it’s a reflection of your personal values and family dynamics. Share your family’s priorities to guide your trustee in decision-making:

- Goals for your children or grandchildren

- Concerns about financial responsibility for family members

- Special needs considerations

- Charitable interests and education priorities

Your trustee should understand the “why” behind your decisions, not just the “what.” This helps them respect your family’s future needs and values.

- Tax-Sensitive Decisions

If your trust involves tax planning, it’s essential to make your intentions clear. Consider sharing:

- Preferences for long-term growth over short-term distributions

- Which assets should remain intact for tax advantages?

- How does your business succession plan tie into tax strategies?

This guidance helps your trustee make tax-efficient decisions that align with your planning and avoid unintended tax consequences.

Information You Don’t Need to Share With Your Trustee

Certain aspects of your life don’t require disclosure to your trustee. To keep things focused:

- Day-to-day business decisions: The trustee doesn’t need to get involved in everyday management unless it directly impacts the trust.

- Personal habits or emotional issues: These don’t affect the administration of the trust and should be kept private.

- Non-relevant relationship details: If certain relationships don’t influence the trust’s direction, there’s no need to bring them into the conversation.

The goal is to provide only the information that will help your trustee make sound, informed decisions on your behalf.

How Often Should You Update Your Trustee?

Regular communication is critical. You should update your trustee whenever there are significant changes to your financial situation, business, or family life. Consider checking in with them when the following events occur:

- Buying or selling property

- Business growth or structural changes

- Family events like births, deaths, marriages, or divorces

- Changes in leadership or debt management in your business

- A shift in your long-term goals

Keeping your trustee updated ensures they’re always working with the most current information, minimizing confusion and preventing errors in decision-making.

How to Protect Your Business Interests Through Trusts

- Protecting Business Interests from Creditors and Family Disputes

While a revocable trust does not protect business assets from creditors, it plays a critical role in business continuity and succession planning.

A well-designed succession plan ensures that if something happens to you, the business does not stall, lose leadership, or face operational paralysis. By clearly defining who steps in, how decisions are made, and how ownership is managed, the trust helps keep the business functioning during periods of uncertainty.

Sharing this information with your trustee such as key contacts, decision-making authority, and transition priorities allows the trustee to act quickly and according to your intent. The goal is not asset protection from claims, but protection against disruption, loss of momentum, and avoidable decline if you are no longer able to lead.

- Involving Business Partners in the Trust

Consider adding your business partners to the trust to outline their role in the company’s future, or their designation as a special trustee. This ensures that their interests are protected and their involvement is apparent.

Create buy-sell agreements within the trust and through a buy-sell agreement that detail how business ownership should be handled if you or a partner becomes incapacitated or passes away.

- Succession Planning for Smooth Leadership Transition

Clearly outline who will take over leadership in the event of your incapacity or death. This can prevent confusion and ensure the business continues without interruption.

Establish specific guidelines in a succession plan for your successor, and provide any necessary training or resources to prepare them for the role.

The Impact of State Laws on Your Trust and Trustee’s Duties

State-specific laws play a critical role in the administration of trusts and can directly influence a trustee’s responsibilities and actions. Each state has its own set of statutes governing trust administration, asset distribution, fiduciary duties, and taxation, which can impact a trustee’s decision-making process.

For example, some states impose different rules on the taxation of income generated by trust assets or provide distinct guidelines for how trustees must report to beneficiaries. A trustee must navigate these laws to ensure they fulfill their duties in compliance with state regulations.

For business owners, state laws can pose unique challenges, particularly in states like California, where laws governing business succession planning and asset protection differ significantly from those in other jurisdictions.

California, for instance, has stringent regulations regarding the transfer of business interests within a trust, as well as specific tax considerations that must be addressed in the trust document. It is imperative to work with an estate planner who is well-versed in the legal landscape of your state to ensure that your trustee’s actions align with both your intent and state-specific legal requirements. This reduces the risk of disputes and legal complications, safeguarding the integrity of your estate plan.

Protect Your Business and Family with a Clear Trustee Strategy

Trustees make better decisions when they understand your goals. You remove uncertainty. You reduce the risk of conflict. You strengthen the transition for the next generation. And you protect your business instead of leaving decisions to chance.

Uncertainty can arise when your trustee lacks the clarity they need to manage your estate effectively. This often leads to:

- Conflicts

- Missed opportunities

- Potential risks for your business and your family’s future.

At Dahl Law Group, we specialize in helping business owners like you ensure that your trustee has all the necessary information and guidance to carry out your plan smoothly. With our clear communication strategy, we align your goals with your trustee’s responsibilities to protect both your business and legacy.

FAQs

- Does my trustee need access to my business records now or only after my death?

- Should my trustee know about assets that are not in the trust?

- Can I limit what my trustee knows while I’m still alive?

- How often should I update my trustee?

- Is written communication better than verbal communication with a trustee?

Dahl Law Group

Latest posts by Dahl Law Group (see all)

- How California’s Single-Enterprise Rule Impacts Your Business - April 24, 2026